The Internet Oversells 72(t)

How it works, when it is applicable, and the potential pitfalls.

Last week on X (Twitter) someone went viral for bashing 401(k) plans. You know the bit, “Why save so I can have $600,000 when I’m old and can’t do anything.” We’ve all seen it.

Tons of people came right back with, “You must not understand Rule 72(t).” While this rebuttal is not wrong, they leave out major context. To me, it seems like they are saying that 72(t) distributions allow for the entire account to be “unlocked” and not subject to early withdrawal penalties. This isn’t the case.

So, I figured we would cover Section 72(t) or Substantially Equal Periodic Payments (SEPP) this week.

72(t), at its core, is a way to access funds within an IRA or 401(k) (if separated from their employer) for individuals below the age of 59.5 without being subject to the 10% early distribution rules.

At face value, this seems like a great way for an early retiree to begin withdrawing from their retirement account in the event they needed to. Honestly, it can be a great way to access these funds! But first we have to discuss some of the mechanics of this election.

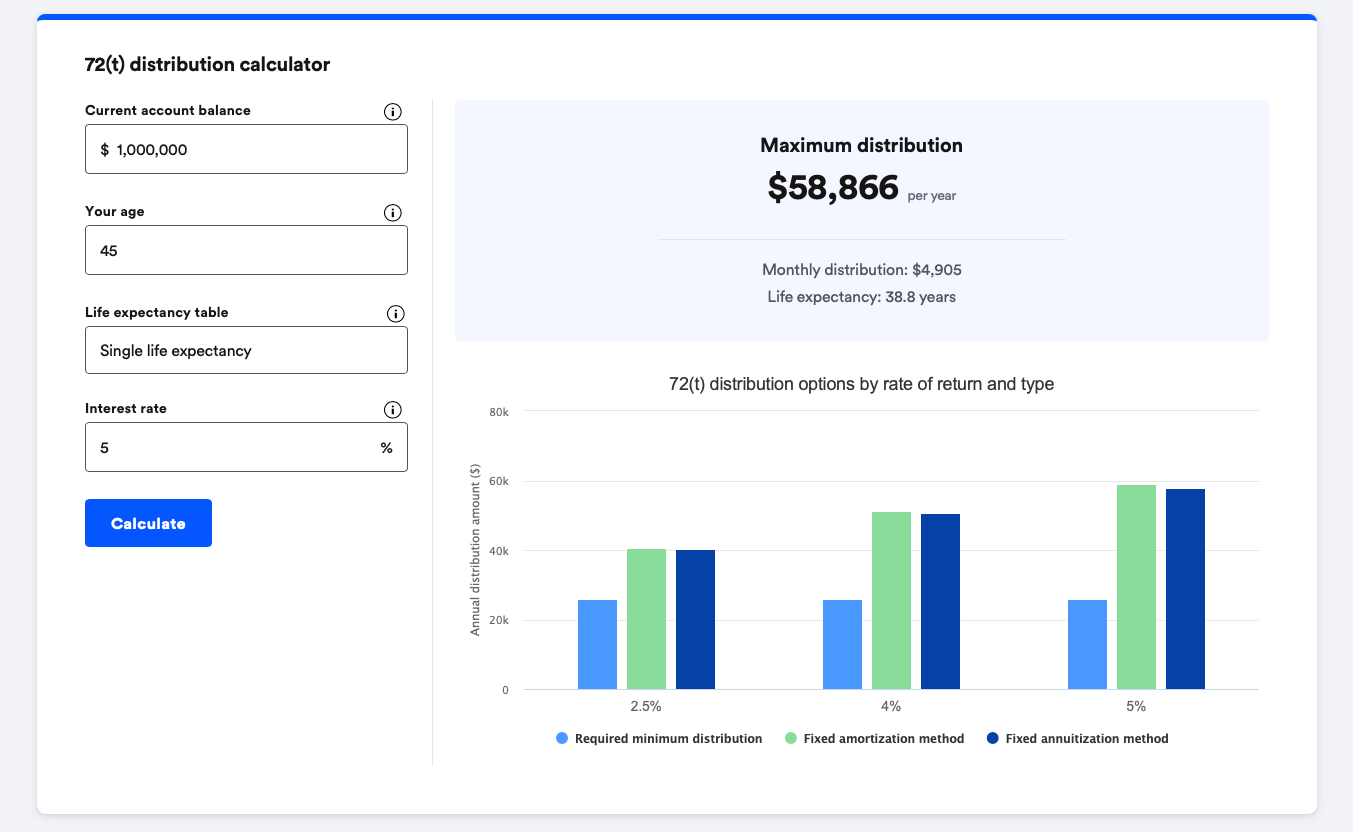

When 72(t) is elected, the owner of the account MUST take distributions annually for the longer of 5 years or until age 59.5. For someone who is 45, this can be a significant amount of time to be required to distribute funds.

There are 3 different methods in calculating the amount to be distributed. These calculations can be a tad in-depth. I will give a brief overview of each and leave a handy calculator below!

The amortization method*: This results in a fixed annual payment and is derived using a reasonable interest rate** and a life expectancy table.

*This method generally allows for the largest annual payment out of the three methods.

**The reasonable interest rate is either the greater of 5% or 120% of the AFR (applicable federal mid-term rate)

The annuitization method: This method also results in a fixed annual payment and is derived through a mortality table offered by the IRS and the interest rate explained above.

The RMD method: This results in a variable annual payment using the life expectancy factors associated with RMDs. This method can result in the most work as the amount needs to be recalculated annually.

Now, I’d like to present the calculator that helps us really visualize how much 72(t) can offer. Bankrate has an awesome one.

For our example, we’ll assume someone is 45, has $1,000,000 in their IRA, chooses the fixed amortization method, and uses an interest rate of 5%. Please note this is just an example and the calculator shouldn’t be solely relied upon if looking to elect into 72(t) distributions, working with qualified professionals is important.

This is where my gripe with the “You must not understand 72(t)” argument comes to the light. Someone who chooses the highest calculation method for 72(t) with a one million dollar balance can access less than 6% of the account’s value without penalty on an annual basis.

And they must do so for over 14 years. Could this be helpful to the right person? Definitely. Does this unlock a significant amount of funds relative to the total balance? Not really.

I’ll also add this, which most online seem to ignore: If any distributions are taken as a lesser amount than calculated or more is taken than the calculated amount, the 72(t) schedule is broken.

This can result in a retroactive 10% penalty on ALL previous distributions. Interest can apply as well.

I am not sure why this potential pitfall is not made more clear when people tout 72(t). Imagine at year 10 in our scenario, after ~$600,000 has been distributed, if the schedule was broken. This could result in the retroactive penalty amounting to ~$60,000 plus potential interest.

Oh… by the way, rolling funds into the account or making an annual contribution can potentially trigger this penalty as well… might be something people would want to know.

Now there are legitimate planning strategies around 72(t) distributions. Unlike for Roth conversions, there is no pro-rata rule and not all IRAs are subject to the rule. 72(t) can be elected for just one IRA of many.

One planning strategy revolves around looking to achieve the highest withdrawal amount from the lowest balance.

This can maintain liquidity outside of the account that is electing into 72(t). So, if a distribution was needed, it can be taken from a separate IRA and the penalty would only apply to that amount, rather than potentially breaking the 72(t) schedule from the initial account.

All of this to say, please double check your sources. Some of these planning topics that are discussed online are more in-depth than they’re made out to be.

While it may seem like I covered a decent bit on Section 72(t) today, there are even more factors that can impact a decision like this.

This is for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.