Fee sensitivity matters. Bring the same energy to tax awareness.

Finding the options that make the biggest impact.

Lately, I have been seeing a lot of fund comparisons online. “Fund X tracks the same index as Fund Y but Fund X charges an additional .06% in expenses!”

They’re not wrong. This can actually make a difference in someone’s investments. Below is an overview highlighting the difference between a .03% expense ratio and a .09% expense ratio. (Each of these are very low). For the example, we’ll take a 7% return and reduce it by the expense ratio.

That could be a solid $47,200 over the course of someone’s investment career. I’m not here to diminish this in any capacity. Optimizing for fees can be an important piece of the puzzle.

However, what I am here to do is show multiple examples of where tax-awareness has much more juice to squeeze than the race to 0% fees.

One issue on this front for some is that the difference in the fee structure above is for a fund that tracks the same exact index. It is much easier to have an “apples to apples” comparison in that regard.

However, there are always tradeoffs. If we do one thing, we don’t do another. So, for the purposes of today’s piece, I’d like to offer comparisons that I’ve come up with on my own. No, they won’t necessarily be apples to apples because there are a billion different things that someone can do with their money. But hey, it’s my newsletter, so I can do anything I want, right?

Tax Advantaged Accounts

You know them. I’ve covered them. Roth IRAs, 401(k)s, HSAs. They can offer significant tax efficiency relative to a standard brokerage account.

I can give you a super easy example of what I am talking about when it comes to tax-awareness having more juice to squeeze with a Roth IRA.

Roth IRAs suffer from no “tax-drag.” Historically, ~30% of the total return for an index such as the S&P 500 has come from dividends. As of recent, this has looked different.

The problem? Those dividends are taxable if held within a brokerage account. Assuming we were working with a high earner, we could estimate these dividends would be taxed at 20% for qualified dividends and tack on another 3.8% for NIIT.

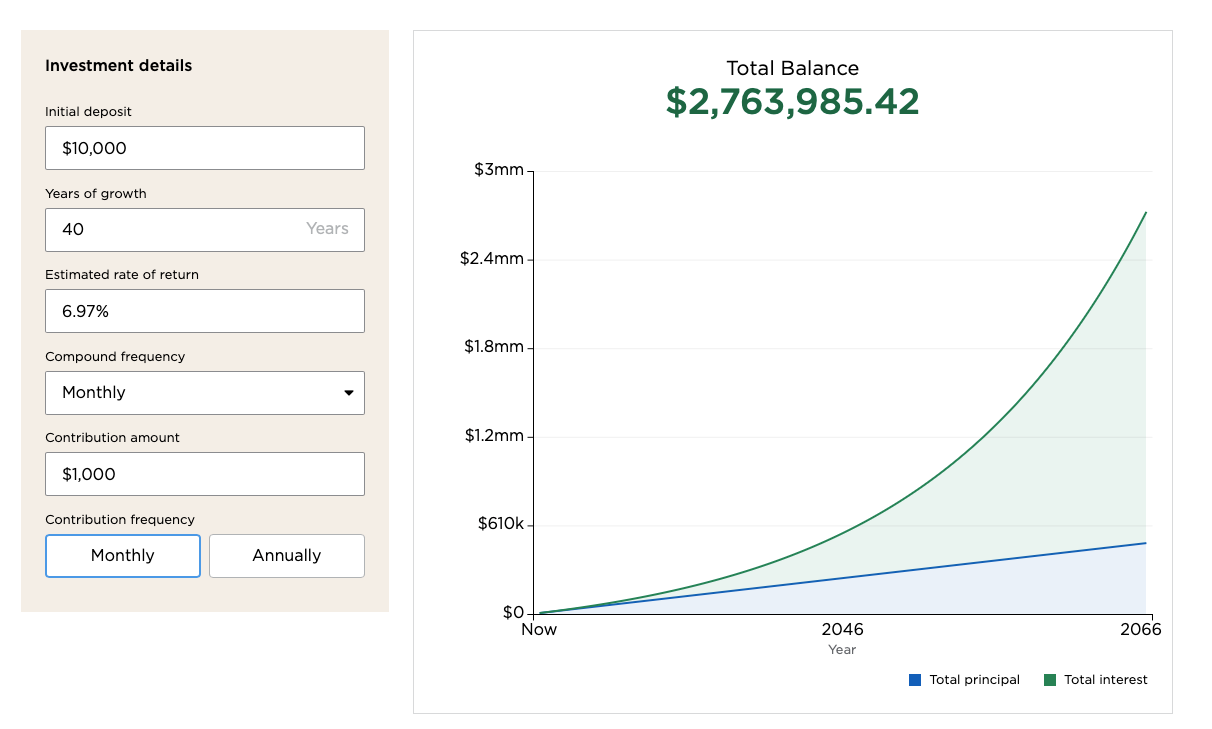

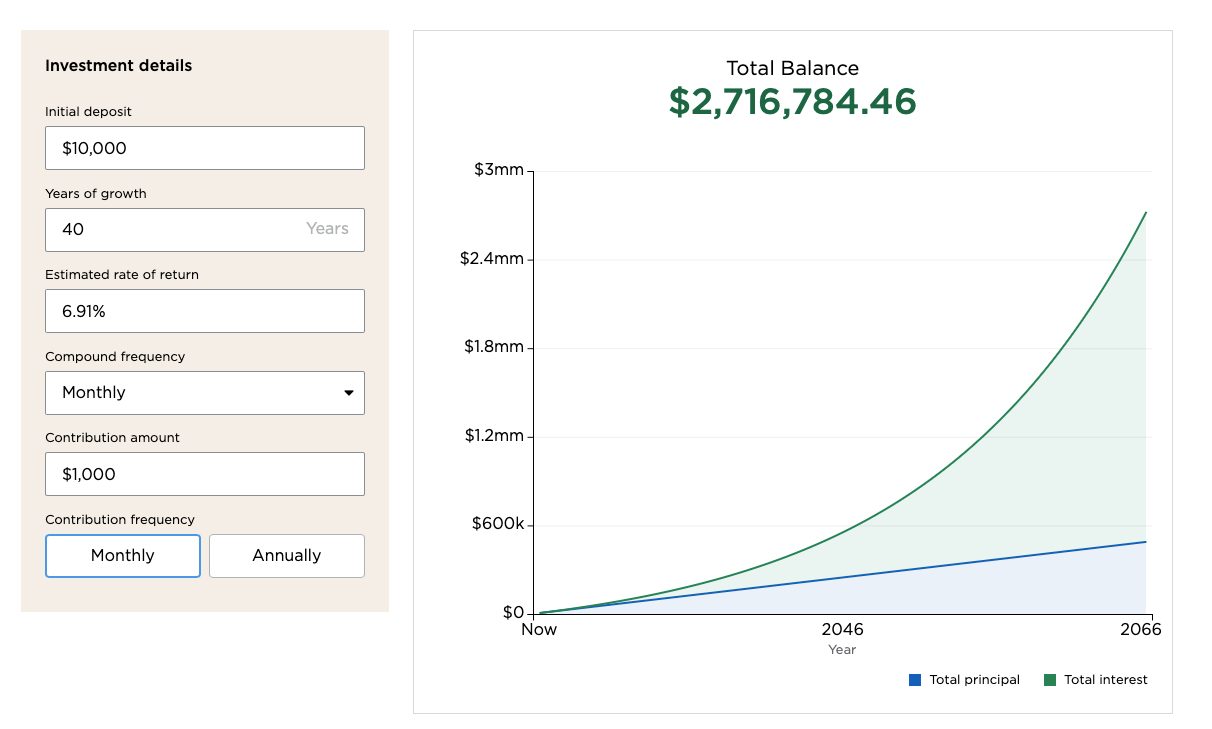

So, let’s work that out now. Assume the Roth IRA and the brokerage are invested identically. 30% of the assumed 7% return is due to dividends.

Our brokerage investor takes a 23.8% haircut on 30% of that return annually. This results in an after-tax return of 6.5%.

See what I mean? That’s .50% annually. Not splitting hairs over a few basis points.

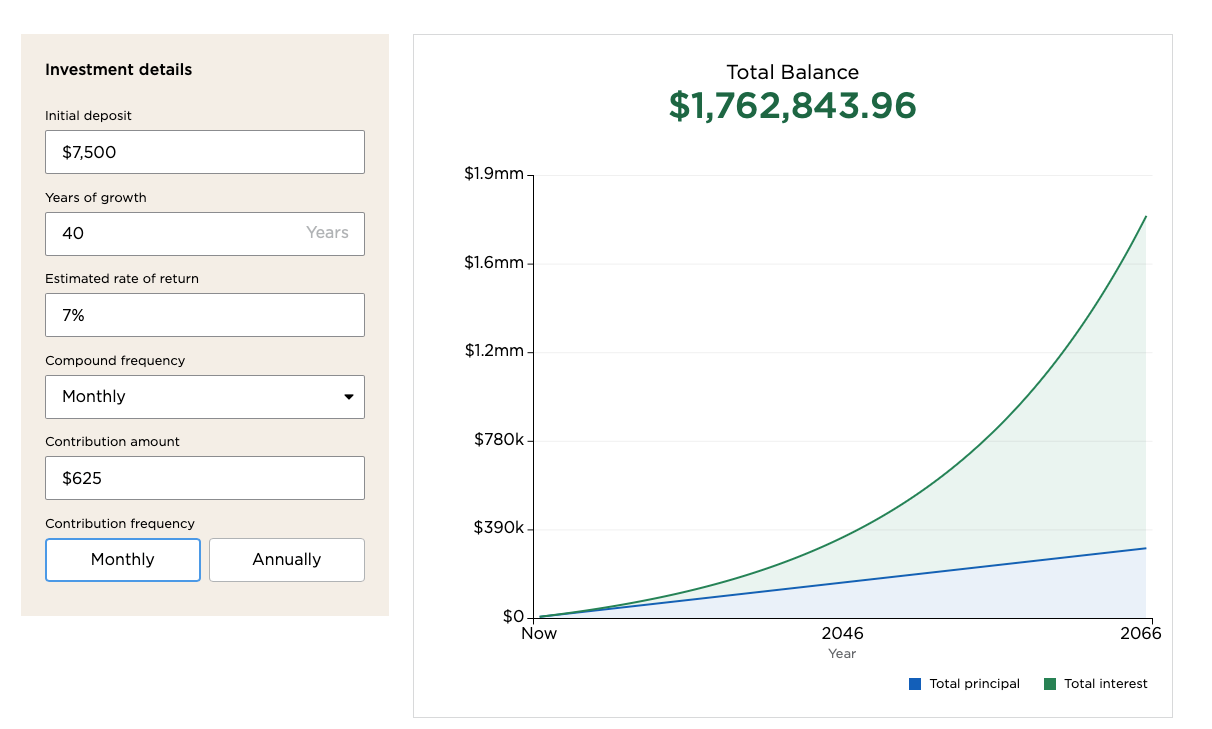

Here’s what the Roth would look like with those variables, assuming monthly contributions of $625.

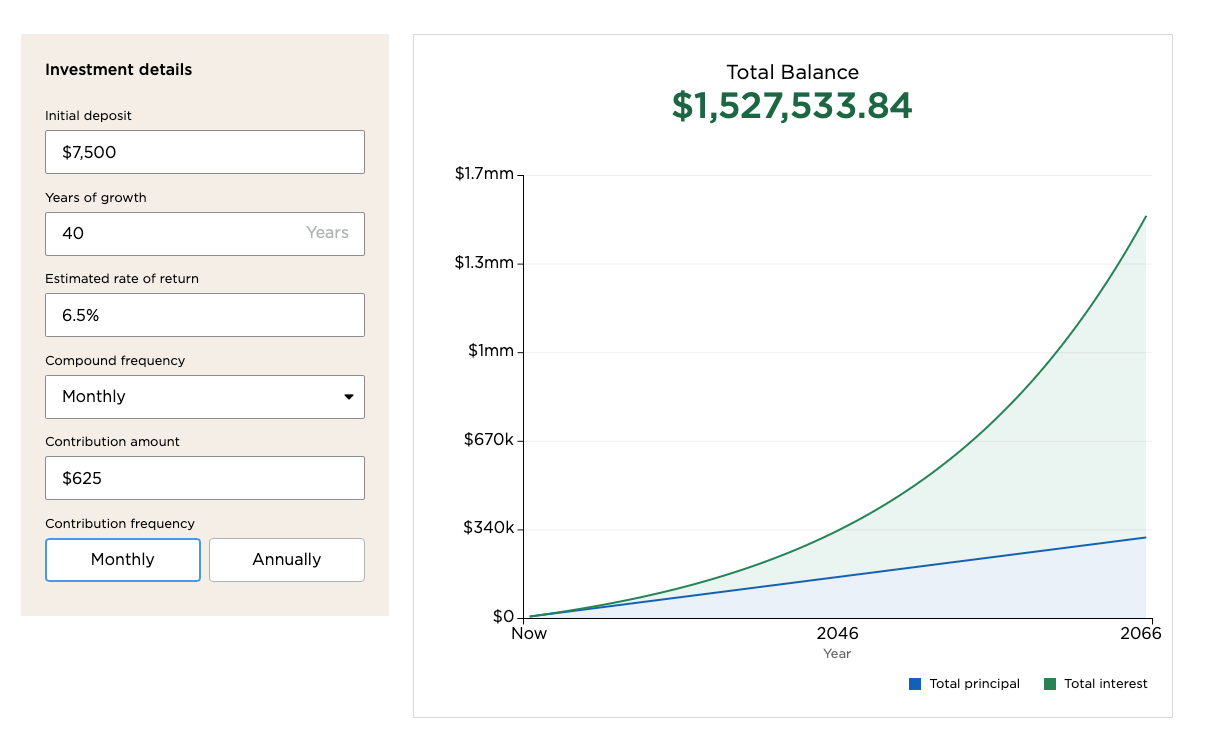

The brokerage? Well, that returned 6.5% net of tax.

We’re talking a difference of nearly a quarter of a million dollars.

Tax-awareness is an ongoing planning item. Take a 401(k) for example.

If someone were in the 37% federal tax bracket, every dollar they get into the 401(k) plan is saving them $.37 on federal taxes.

And some might say, well, if they chose Roth, they’d never have to pay taxes again on it.

Sure, that isn’t wrong but the pre-tax saver could very well create tax arbitrage. Imagine contributing to avoid the 37% bracket for years and distributing the funds when the individual’s bracket dropped to the 22% federal bracket.

That is a 15% spread that the individual effectively captured by simply being aware. Being aware of how to arbitrage the brackets can allow for a much more holistic understanding of where to look to put the next dollar is important.

Which Accounts to Use:

On the same note, let’s consider an individual who contributes up to the match in their 401(k). They also have an HSA. Now, they are considering where to allocate the next dollar.

Well, the HSA, if a Section 125 Cafeteria Plan, allows for an individual to avoid FICA taxes. This is your standard 7.65% employees pay towards Social Security and Medicare.

Directing additional funds to the 401(k) won’t save the employee anything on FICA. Yet, it can be an automatic boost if they directed funds to their HSA relative to the 401(k) plan.

That’s a significant boost too! Talking about over 7%, just for being aware!

Using Opportunities to Get More

If you’ve been reading my newsletter for a little while, you know that tax-loss harvesting can be something worthwhile. This income shifting tactic can allow for an individual to capture losses and use their economic value today.

This strategy is largely valuable. Don’t believe me? Check out what the hedge funds are up to. Their pivot to tax-awareness should be studied (don’t worry, I am actively studying this).

Losses can move the needle so much that many people are looking to direct indexing, or even, tax-aware leveraged long/short strategies that exacerbate the losses even further.

Achieving additional tax-alpha through loss harvesting can be something that moves the needle. Arguably more so than the difference between paying .03% and .09% for an expense ratio. In many cases, ultra-high net worth clientele are paying wayyyy beyond that in management and operational fees associated with the leveraged long/short strategy.

Before this turns into a book, I’ll stop myself here. If there is one thing the Tax Planning Certified Professional® coursework taught me, it’s that almost everything can be optimized for taxes. There are angles I was previously blind to that I am implementing in every plan I deliver lately.

Of course, fee sensitivity is important, but tax-awareness likely has much more juice to squeeze. The toughest part of tax-awareness is that it is incredibly subjective. It is not as simple as finding similar funds and choosing the cheaper one. It is about a holistic approach to mitigate taxes throughout one’s entire life.

The vast majority of people have one expense that tops them all. It’s not a home, it’s not a car, it’s taxes.

Next time something comes up in your financial life, I encourage you to dig a little deeper on the tax front. You might be surprised with the outcome and what you learn.

This is for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.